Techmind - Proptech Barometer 2nd Semester 2021

Analysis of structural and cyclical trends in the Proptech sector on a Global, European and French scale.

For several years, the Proptech sector has sparked a great interest and new trends have continuously emerged to revolutionize the sector: coliving, virtualization of housing visits, real estate crowdfunding, digitalization of construction management, etc.

Our study on the 2nd half of 2021 (available here) is a quantitative demonstration that confirms all of these structural trends as well as other trends related to the impact of the economic situation on the sector.

Through this semi-annual barometer, our purpose is to inform the investment decisions of investors by answering questions such as :

What are the most attractive areas for investors?

What is the degree of maturity within the various components of the Proptech value chain?

Who are the new emerging leaders on a Global, European and French scale?

What are the latest trends in mergers and acquisitions?

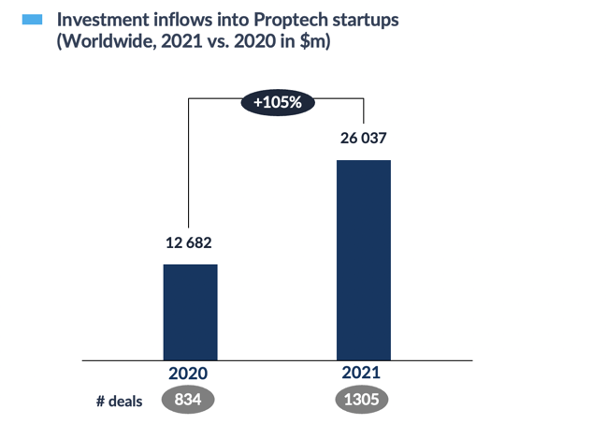

New highs in fundraising

The economic potential generated by these multiple innovations can be gauged by the strong increase in the number of fundraising rounds (+56% compared to 2020), as well as the achievement of mega funding rounds (e.g. WeWork funding round of $950m, the largest amount over the period).

Nonetheless, it is crucial to note that the first argument must be qualified, as this increase is being driven upwards by the return to a more favorable health and economic situation in 2021.

Due to these two arguments, the total amount raised by Proptech startups in 2021 has achieved a 3-digit growth (+105%) compared to the previous year.

We shall see how this develops in 2022, as a new crisis is now beginning.

Source : Crunchbase

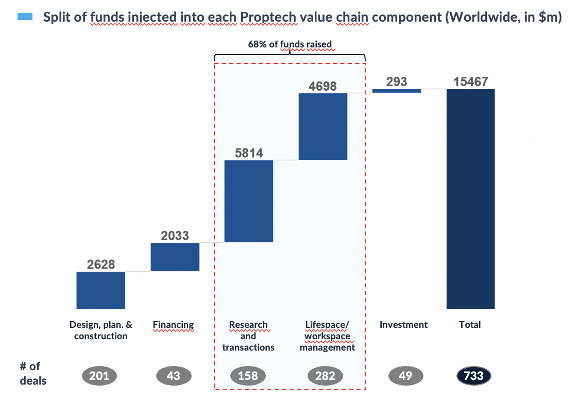

The predominance of startups dedicated to management

During the course of our study, we also noticed a resurgence of technologies belonging to the "Lifespace / Workspace Management" value chain.

Indeed, 38% of the deals completed (representing 30% of the amounts raised) were dedicated to startups belonging to this value chain.

Source : Crunchbase

In an interview granted to Crunchbase, Fatima Dicko, the founder and CEO of Sugar, a Proptech startup that aims to turn apartment buildings into interactive communities, explains that this trend comes from the interest of Generation Z in new technologies and more specifically in smart home technologies

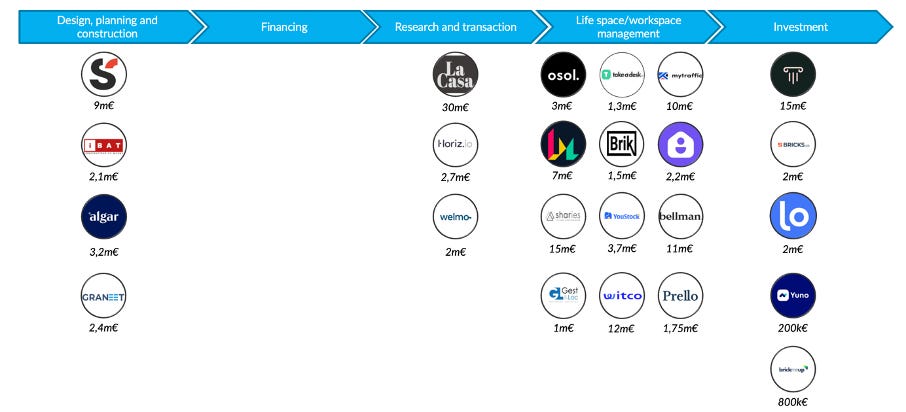

For instance, half of the French startups that have raised funds over the period are dedicated to facilitating property management.

Overview of French fundraising by value chain. Source : Crunchbase, Press articles

There is also an upsurge of startups providing solutions to outsource various tasks necessary to housing or management of rental property. For example, Bellman, Prello or Brik, three French startups that meet this need, have raised funds in the second half of 2021.

Surge in M&A Deals

Finally, the number of M&A deals is also booming across the globe. Indeed, many startups have reached a sufficient level of maturity to be willing to acquire other startups in order to expand into other parts of the value chain, and thus diversify and expand their activities.

Furthermore, this trend is likely to intensify in the coming years.

Although most of the M&A transactions involved startups belonging to the same value chain, we observed that there was a very narrow line between the Research & transactions and Lifespace/ workspace management value chain components. Indeed, many startups operating in one of these two value chains have acquired a player from the other value chain in order to widen their scope.

This is for example the case of Spruce, a provider of lifestyle services to the multifamily sector, which recently acquired The Minte, a start-up that brings hotel-style housekeeping to luxury apartment residences. Through this transaction, Spruces’s goal is to strengthen its presence in Chicago, while offering The Minte the ability to scale and serve more clients.